Update for Childminders on MTD and the 10% Wear and Tear Allowance

Since our last post about the confusion over the alleged removal of the 10% wear and tear allowance when using Making Tax Digital (MTD), we have been in contact with Senior Policy Advisors at HMRC to try and understand any forthcoming changes for childminders.

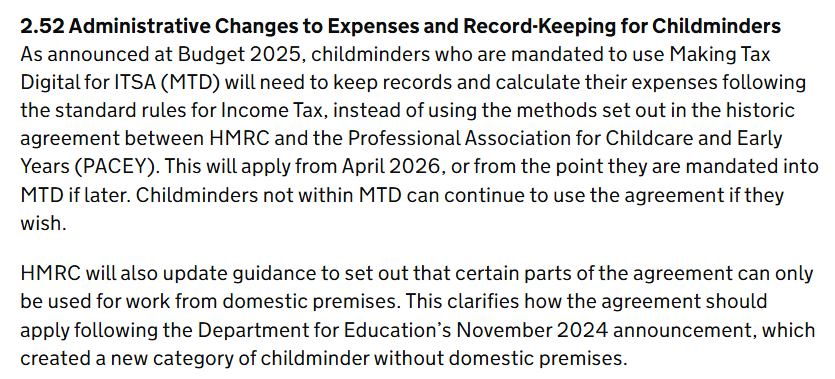

The 154-page Budget 2025 document, published on 26th November 2025, did include the following:

A further HMRC document, Budget 2025 — Overview of tax legislation and rates (OOTLAR), published on 5th December 2025, provided some more details:

What does this mean for childminders?

Essentially, the longstanding HMRC agreement that has been in place since 2013 will be disbanded for childminders who use Making Tax Digital (MTD) although there is absolutely no mention of this on the HMRC website page about the agreement (BIM52751), which was last updated on 3rd December 2025.

When do childminders have to use Making Tax Digital (MTD)?

It varies depending upon your income, but it ranges from 6th April 2026 to 6th April 2028.

If your childminding income is over £50,000 you must use MTD from 6th April 2026.

If you work on your own as a sole-trader and your childminding income is between £30,000 and £50,000 then you must use MTD from 6th April 2027.

If you work on your own as a sole-trader and your childminding income is between £20,000 and £30,000 then you must use MTD from 6th April 2028.

So the 10% wear and tear allowance is being removed?

Yes, as far as we know, from the date you use MTD, but you can still claim the 10% wear and tear allowance until that point.

That doesn't sound fair?

We agree. It will create a two-tier system between 6th April 2026 and 6th April 2028, where some childminders will continue to benefit from the agreement and others will not. Even if it were a level playing field, and all childminders had not follow the same rules, it is still unfair for childminders who have been used to benefiting from agreement over the last 12 years.

What about the other aspects of the agreement?

It looks like other aspects of the agreement, such as those in relation to heating, lighting, water and council will continue to apply, but the specific rates and allowances may change. We are still awaiting confirmation.

Is there any alternative to the agreement?

Yes, but it might be less generous for many childminders, although better for others.

HMRC told us:

"All self-employed businesses can claim tax relief for costs of purchasing, repairing, and replacing items, including via capital allowances. The current administrative process available in our guidance for childminders, specifically for furniture and household items, is to deduct 10% of their total childminding income from taxable profits instead of using actual deductions. Under MTD, childminders must use actual expenditure, aligning with the standard rules. However, this alignment will be phased in from 2026 to 2028, in line with the MTD thresholds.

Childminders can deduct many other costs, such as utilities, cleaning and equipment, as long as they are incurred for business purposes. We do not provide an exhaustive list, allowing flexibility for childminders to decide which costs they have incurred wholly or partly for business purposes, based on their own individual circumstances. It could be that getting tax relief for the actual costs incurred may be more beneficial to childminders, so the expenses associated with the valuable work they do are reflected in their tax calculation."

What does that actually mean?

Essentially, instead of claiming the wear and tear allowance and other deductions allowed under the agreement, a childminder, in theory, will be able to claim for the costs of of purchasing, repairing, and replacing items used for their business.

In the case of items used for both personal and business use, a childminder may be able to claim for a proportion of the cost.

It sounds really complicated?

The rules are more complicated to understand and complex for childminders who use some household items for both personal and childminding purposes.

It will make a childminder's tax return and accounting more complicated under MTD.

What are Childcare.co.uk doing about this?

We understand childminder concerns and are actively campaigning and talking to HMRC senior policy advisors in an attempt to get the decision to remove the agreement overturned.

If the government are set on their changes, we have asked HMRC to provide clear and easy to understand information for childminders, with examples of what they can and cannot claim for, together with information on how to claim for items used both for their childminding business and personally.

We will continue to speak with senior employees at HMRC and the wider government, and will issue updates as soon as we have more information.

How can I contact HMRC for more advice?

You can contact HMRC for more advice about the changes.

Don’t have an account? Register free today

Create a free account

Sign up in one minute, no payment details required.

Member benefits include:

- Add a free profile detailing your requirements or services

- Search by postcode for local members near you

- Read and reply to messages for free

- Optional paid services available